We are excited to share with you our latest research report on Copart! As always, we have released it concurrently with a shorter summary. If you are short on time, we recommend starting there. Please email us at info@speedwellresearch.com for any questions, concerns, or comments. See our full disclaimer on our website.

*Figures refer to fiscal years, which end in July.

Founding History.

Born in Oklahoma in the 1940s, Willis Johnson spent most of his youth ping-ponging around the country as his dad worked odd jobs and sifted out unique opportunities. His dad wasn’t against manual labor, but he spent most of his energy searching for business opportunities in the local paper. One such opportunity landed the Johnson family ownership of an Arkansas dairy farm. Willis learned the value of discipline and the importance of hard work first-hand as he attended to their cows and the farm whenever he wasn’t in school. He recalls waking up at 3:30am to milk the cows, driving into town to hit the creamery by 6:30am before attending school, then returning to the creamery to pick up the empty cans after school and milking the cows again in the evening. However, it wasn’t too long before his dad auctioned off the farm and they wound (back) up in California.

Willis’ mom would read the classified ads to his father who was illiterate but analyzed each business opportunity. One of his more notable business endeavors was when he bought the assets of a bankrupt construction company and tasked the young Willis and one of his friends with dismantling their equipment and inventory into portable pieces of metal. The plan was to simply sell it for scrap iron and move on, but Willis’ dad realized he could regularly buy cars for $5 and scrap them for $17, so they stayed in the dismantling business. Soon enough, they had to get a farm to store all the junk and get the requisite permit after the city hassled them: they then officially owned a junkyard.

Willis would learn a great deal not just about how to dismantle cars, but also things like what each part could be worth and what to look for in a wrecked car. This learning was eventually put on pause though, as he enlisted to serve in the Vietnam War. As a forward observer in the army, it was his job to stand out in front of the unit and check for ambushes and booby traps. He saw horrendous action: half of his unit was killed. All of the survivors received Purple Hearts, which are awarded for sustaining injury in the line of duty. Willis would pull mortar shrapnel out of his body for years afterwards. After leaving Vietnam a year later, he threw his Purple Heart in a drawer and didn’t think about it again for decades.

After returning home, Willis resumed work at his dad’s junkyard until quarrels with his increasingly drunk father led him to strike out on his own. He started working at Safeway, a supermarket, before eventually finding a junkyard whose owners were set to retire. He convinced them to take a fraction of the $75k asking price as a down payment with interest-only payments in the interim. To save money, Willis and his wife moved into a trailer on the property. It was named Mathew Auto Dismantlers, after the nearby air force base.

Initially, Willis focused on scrap metal. He would find cars that were so beaten up that they had no longer had any value as a car, and then melt them down to sell the raw materials. However, many of the cars he bought still had some working parts, which could be resold to DIYers or mechanic shops at a premium to melt value. In order to build out the parts side of the business, he focused on getting higher quality cars (keep in mind “quality” here is relative to literal junk). Willis had a few novel insights though: instead of selling parts in their entirety, like an engine, he would break them down into their constituent parts. Whereas a competitor would sell an engine for $400, he sold the distributor, alternator, carburetor, etc., individually, and could get $700 for the same engine, only dismantled. Additionally, selling parts individually meant he wouldn’t have to guarantee the whole motor worked, especially if it broke soon after a sale. Willis would also clean the parts and paint them when necessary to make them look new. He would then display them in a retail format store with shelves instead of strewn around a yard like competitors did, which further garnered an additional premium for the parts.

The next thing Willis did exhibited his innate business savviness. In order to differentiate himself, he specialized in specific car parts. However, instead of picking the most popular models, he picked items that specifically weren’t “hot-selling” products. He chose to specialize in Chrysler, Dodge, and Plymouth parts. Dismantlers thought he was foolish, but were nevertheless happy to sell him their slow-moving parts, and also refer customers in search of those.

By specializing, he could serve a customer need that competitors not only weren’t, but had no desire to address. Focusing on items his suppliers didn’t want to carry allowed him to get good pricing, while simultaneously generating customer referrals from these suppliers. Customers were more willing to drive far out to get their Chrysler or Dodge products since he was the only supplier in the region. Essentially, by focusing on “slow-moving”, unique parts, he could actually make them turn faster. By specializing, he was able to increase the geographical reach of his yard and make the assortment of goods turnover quicker while simultaneously insulating himself from local competition since he had a differentiated offering. These changes worked in a big way: his sales jumped to $3,500 a day to $3,500 a month.

As his business grew, he needed more inventory. He started visiting Bob’s Tow Service, also known as BTS Auctions, who would tow totaled cars on behalf of an insurance company and then auction them off to local dismantlers, car rebuilders, and mechanic shops. (A totaled car is a vehicle that incurred damage and the insurance company deemed it would be cheaper for them to sell the damaged vehicle and pay the policyholder a settlement instead of trying to repair the vehicle. A totaled car may also be called salvaged). Willis would spend $10k a week on salvaged cars to haul back to his yard.

With his yard swelling with car parts, he spent $110k on a computer, which he later noted cost more than two houses at the time. However, it was more than worth the investment, as it allowed him to keep track of all of his inventory at a time competitors were using a flurry of paper and file drawers. It taught him which parts of a car to scrap and which he should stock more of across thousands of different parts that varied by make, model, and year. (He would later also build a computerized system for the California DMV. Since the manual title transfer processing was forcing him to store cars on his lot for weeks longer than ideal, which ballooned his working capital, he developed an electronic solution, at his own expense, for the DMV that cut weeks out of the process).

Showing his entrepreneurial nature, Willis opened up several related junkyard auto businesses around then, including: 1) a minitruck-focused junkyard, 2) Today Radiator, which focused on used radiators, 3) a used auto-parts-focused store, 4) a foreign-car-focused junkyard, and 5) U-Pull-It, which operated yards full of damaged cars that customers pulled parts off themselves, making it the cheapest way to buy parts.

He even started a dismantling magazine so he could advertise to more repair shops, insurance companies, and mechanics. Thinking back to his farming days when farmers would store grain together in a co-op, he thought the magazine was a similar concept since there was a “co-op” of parts dealers using the magazine. He decided to call it Copart.

After some time, Willis became BTS Auctions’ largest buyer, and while it was an important source of vehicles for him, the owner wanted to retire and his kids wanted to sell the business. They wanted $1mn for the business, even though it had just $100k in equipment and brought in $65k pre-tax. However, Willis knew BTS Auctions had basically been on autopilot for years, and that there was enormous growth potential. He had also thought that when a business is family owned, salaries and other family expenses were included in the financials, which he would not have to incur. As such, he partnered with Peter Kay, a friend of his, each putting up $50k as a downpayment, to purchase the company. Since Willis had to use his other businesses as collateral, he got a controlling 51% stake. In 1982, he became the proud owner of his first car auction.

The recession in the mid-70s crippled advertising revenues from his Copart magazine, and since it was already legally incorporated, he decided that rather than pay to set up a new legal structure for BTS, he would use the magazine’s existing one. Copart Auctions was born.

Business History.

While Willis was focused on all of his different automotive businesses, Peter was in charge of Copart’s day-to-day operations. In short order, they opened a second Copart yard in Sacramento. They realized that the shorter the distance each car had to be towed to get to a yard, the cheaper it would be to service that unit, so they kept looking to add locations. Their third yard was opened in Richmond, San Francisco.

Peter, however, was quickly approaching 70, and spending more and more time with his racehorses over Copart, and it started to show. When a few lapsed bills were overlooked, Willis had enough. Willis gave Peter an ultimatum: They would each write a number on a piece of paper, and Peter could buy the business at Willis’ number or sell at his own. Peter sold.

With Willis now fully in charge, he started making changes. Sealed bids were changed to live auctions. Guests were allowed to come in so long as they could get a licensed dismantler (a requirement to bid on salvage pool cars) to take liability over them. And he kept adding yards as opportunities presented themselves.

The biggest business transformation was a change in the incentives and economics of the auction business. Just as cleaning the car parts he sold increased the price he could command, doing the same for his salvaged cars yielded a similar result. He wanted to make the cars look nicer, but knew the insurance companies would be reluctant to spend money on this. So instead, he thought, what if there was a way to split the increase in price from making the cars look nicer?

At the time, it might cost about $200 to pick up, store, and auction off a car. Willis wanted to instead incur that cost, plus the cost of cleaning up the car, in exchange for a percentage of the proceeds once the car sold: 20% for old and highly damaged cars and 10% for everything else. The result was that both the insurance companies and Copart generated higher proceeds.

This arrangement, which Willis called the Percentage Incentive Program, or PIP, also solved another issue insurance companies had. A burned-out car may have fetched only $25 in an auction, but cost that same $200 for Copart to pick up and process. The insurance companies were losing money on each of those units. Under PIP, Copart instead would be the one to lose out on that car by incurring expenses less than their portion of proceeds. The kicker is that Copart would only offer PIP if an insurance company contracted out all of their cars in a region to Copart. So Copart would lose on a fire-damaged vehicle, but make it back on a lightly damaged, newer car. Economics aside, Willis liked how he was now aligned with his customers: they both wanted the highest price for the cars, whereas before his revenues only increased with volume.

In 1989, he met Jay Adair, a recent high school graduate, and his daughter’s boyfriend. Jay showed a curiosity in the salvage business, partially driven by his amazement that anyone could make money from junkyards. He would pepper Willis with questions about the business, and before long, Willis was taking Jay with him to investigate new properties for purchase. After Jay’s first year of college, he decided it wasn’t a good use of his time and that he wanted to become a businessman. When he told Willis, Willis handed him a broom.

Jay started running more of Copart, starting with the titling department that interfaced with the DMV, and then moving to the customer service department. He excelled at work both in the office and out in the yard, but he was worried that Copart could never grow to the size that it would be big enough for him to take on meaningful responsibility and make a lot of money. That all changed in 1991, when IAA, an auto auction competitor, went public. Flipping through the prospectus, Willis thought that if IAA could do it, then so could they. He traditionally eschewed debt, but liked the idea of raising capital that he wouldn’t have to pay back. He recalls thinking that “going public would allow Copart to not just grow—but grow big”.

Before going public though, they had to get larger. So he got in touch with a Wall Street investment banker to help raise $10mn in a private round. He was able to raise that amount as a convertible that paid 8% interest and would convert into a 26% stake of the company. Willis and Jay then embarked on a growth phase, tripling their footprint to about a dozen yards and generating $1.4mn in EBIT on $10mn in sales.

That was enough that their banker thought they could complete a public offering. They sold 2mn shares at $12 a share, raising over $20mn after underwriting fees. Whereas just a few years earlier the whole operation was only a few local locations, they were now a New York Stock Exchange listed company valued at over $80mn. Willis’ 40% stake made him wealthier than he could have ever dreamt, but he was just getting started.

The proceeds were their ammo, and Copart was prepared to go to war with IAA. They would try to swallow up as many mom & pop junkyards, as well as several regional chains, as quickly as they could, as they knew IAA was breathing down their neck.

Whereas Willis often made handshake deals to come back and sign contracts on the hood of a salvaged car in cowboy boots, IAA showed up in limos with lawyers in suits. The IAA approach turned off some junkyard owners but impressed many others. They battled for acquisitions as the industry rapidly consolidated. By 1996, Copart had 49 locations. Revenues grew to a sizeable $118mn and $18mn of EBIT. This growth, though, was funded by a near doubling of shares outstanding, as they used their stock as currency to acquire more properties. This included a secondary offering at $19.25 in 1995 that raised an additional ~$30mn.

With many junkyard locations hard to replicate because of permitting requirements, land scarcity, and the public generally against allowing a new junk yard to open up anywhere near them, the race was on to acquire properties in as many markets as they could. However, whereas IAA was privy to buying big and expensive lots in large cities like Chicago for $7-9mn, Copart would opt for smaller suburban yards in Longview or Lufkin for $1.5-2mn. Copart was focused on building a network more than buying any one namesake location. They thought more locations would allow them to tow cars a lower distance, which would make their operation more efficient, even if it came at the cost of losing some city-center business for the time being.

Interestingly, despite IAA being bigger, Willis was often winning bids against them because IAA bought companies “the Wall Street way”, based on accounting earnings. Willis, on the other hand, knew that a lot of these family-run businesses would use the company as a sort of piggy bank to buy personal cars or pay salaries to family members who didn’t work much (something he learned when he originally bought BTS Auctions). As such, Willis would size up how many cars they sold at auction and what he thought Copart would make if they owned it. IAA thought more in terms of how an acquisition would look from a pro forma GAAP perspective.

A big difference between Copart and IAA was what they did after acquiring a property. IAA would more or less leave it alone, thinking it was more urgent to acquire the next property than integrate the one they had just purchased. In contrast, Copart would train staff members in the Copart way and change operations so each yard would run the same. At one point, they even slowed growth to focus on unifying all of their properties into a single ERP (Enterprise Resource Planning) system. It took two years and $3mn, but by 1997, they started rolling out their new computer system yard by yard. This made it much easier to manage the increasingly national operation, and keep track of and identify any particular yards that had abnormal inefficiencies.

Copart’s readiness to adopt technology and experiment has always set them apart from their competition. In the late 90s, Jay started hearing about “.coms”. At first, he thought they could list their cars online to limit the paper they were wasting—it took over 8,000 sheets of paper to circulate the weekly auction list of cars.

But then he realized that they could use the internet to help solve one of their largest pain points: buyers were hiring people to bid on their behalf at the car auctions, paying them $150 every time they won a car. He thought it was silly that people could make $2-3k a day just standing around and raising a paddle. This was a prime use case for the internet to serve—buyers could come the day before and view the cars, then place a bid online for $35 instead of paying a contractor to stand in the live auction. Jay was right. Copart’s online platform generated $1mn in sales the first quarter it launched.

There was one particular transaction that stood out, and in retrospect, anticipated a multi-decade shift in how cars would be purchased. The auction winner of a car sold in San Diego was a buyer in Connecticut. Whereas cars were always sold locally, maybe occasionally regionally, this was an instance of someone buying a car across the country, sight-unseen. Jay called up the buyer, and he said that while he knew what he was buying, it would be helpful if Copart added pictures online. Jay proceeded to buy 55 cameras and teach each of Copart’s General Managers how to take pictures of a car. With photo listings set up two quarters later, that $1mn of online sales per quarter grew to $10mn, and they closed 2000 with a total of $190mn in revenues.

Still though, bids were not being placed live during the actual auction, only prior. The first iteration of online bidding was born in 2001 and dubbed Virtual Bidding 1 (VB1). It required building out large structures to house the auctions inside with large TVs that showed pictures of the current car. No longer were auctions held out in the open in the yards. The internet system was linked to a row of employees at computers who would monitor online bids and signal to the auctioneer if there was an internet bid. This allowed the internet bidder to be enmeshed in the live auction happening on the floor.

With online auctions, the thing they noticed was not just that buyers from far away markets were participating in the auctions, but that the auction prices were increasing. This meant higher returns for the insurance company and a higher cut for Copart, since over half of their cars were on the PIP model. (“Returns” is industry terminology for the sales proceeds as a % of average cash value or pre-accident value. If a car is worth $10k before an accident and Copart sells it for $3k, then that is a return of 30%).

When 9/11 hit, financial markets were spooked and there was a fear that people would be reluctant to travel again for a long time. Planes were flying at just 5% capacity. Willis and Jay were on a flight to visit a yard with just a handful of passengers, but when they got off to rent a car, they noticed it was slammed. Willis realized that miles driven would go up as people avoided flying, but he lacked the cash needed to continue their yard acquisition spree. They had over 70 locations by then, but in order to continue growing, he went back to Wall Street for another secondary offering, this time raising $116mn at $29 a share.

VB1 was creating operational issues though, and further growth almost assured it would only get worse. The employees that monitored the online bids couldn’t watch the screens for more than an hour at a time without error rates skyrocketing. Their largest yards still had yet to incorporate the system for fears it would be too hectic and bids would get lost. Buyers stopped coming to the yards in-person to bid online, which interfered with the live competition component. Taking the middle option of quasi-online and in-person was an optimization of mediocrity. Jay told Willis they would either have to go all in on the internet or abandon the effort.

In deciding what to do next, Willis turned to a framework that Clay Christensen popularized, despite likely having never read his business literature. “Ask yourself, what’s my job?”. He thought back to his time as a buyer in salvage auctions, which required spending half of his time traveling and standing in line to bid, and he realized that this technology would both cut all of that hassle out and allow a bidder to potentially make more money since they could easily see more cars. He knew buyers would benefit from it, but when it came to defining what “job” Copart did, he decided it actually wasn’t about the buyer, but rather getting the most money for the insurance companies. Reducing buyer friction was a means to that end.

VB2 got its name for it being the second generation of virtual bidding. Instead of integrating the internet auction with the live auction, the entire thing would be run online. Similar to how eBay worked, buyers would place their max bids and the system would bid on their behalf up to that amount. Buyers could still walk the yard to see the cars, but the live auction was replaced with computer booths to submit electronic bids. This solved all of the operational hiccups that juggling parallel systems created. Below, Willis notes how in retrospect, he should have been more hesitant as the VB2 implementation essentially rearchitected their entire business model. There was no institutional paralysis though. In just 90 days, they uprooted their entire operation and converted all 94 of their yards to VB2.

Alongside reinventing the bidding operations, they experimented with a few other new businesses as well. They launched a separate “off-site” vehicle auction platform for sellers to take a photo of their car and post it online without it ever going to a Copart location. They also created “Motors Auction Group”, after an acquisition of a Detroit facility, which was focused on selling nondamaged cars to the public. The idea was to create more of a consumer-focused marketplace to sell higher quality cars, perhaps leveraging some supply from bank repos and their dealer relations. Additionally, they rolled out a wholesale auction initiative that would focus on dealer-to-dealer auctions. (This is especially relevant for when a dealer gets a trade in for say an Audi, but they are a BMW-branded dealer. They would have a tougher time selling that Audi, so selling it to another dealer is usually the most economic move).

By 2006 though, they shuttered all of these initiatives, and it wasn’t because they weren’t good ideas. In fact, there are many businesses focused on each of these areas today, but that was exactly what they realized. It would be very costly to embark on these non-core areas that enjoyed none of the moats their salvage auctions did and had low barriers for competitors to enter. After a few years experimenting, they shut down the public auction and wholesale business. They noted that there were more difficulties than anticipated in growing that business, and the returns were worse. This episode showed that they were willing to experiment but would quickly shut down anything that didn’t show a promising return on investment.

There was another event that happened a year prior that also helped feed the decision to focus on the core: Hurricane Katrina.

When the Category 5 Hurricane ripped through the Gulf Coast states, it left devastating damage and prolonged flooding. More than 300,000 cars are estimated to have been salvaged in the aftermath. Copart’s yards, however, were not large enough to deal with the surge in volume. The local sub-haulers they hired to move cars were at full capacity, but there were still tens of thousands of cars assigned to them that had yet to be addressed. So, they paid extra to bring in almost 300 additional sub-haulers from across the country. In order to find vehicle storage space, they rented out extra plots of land and spent millions on new equipment to handle the vehicles. As Jay Adair noted in 4Q05, “Our primary purpose right now is getting the cars in as quick as we can, servicing the major carriers. And will we make a profit on this? Probably not.”

Rather than taking the catastrophe as an opportunity to increase prices on desperate customers with no alternatives, Copart instead maintained normal pricing. They didn’t pass through any of the millions in incremental costs associated with the CAT to their customers. Not only did Copart competently manage the record influx of cars, but they also built significant customer goodwill for not being opportunistic. A competitor who wants to steal a contract from Copart in the future would also have to convince the customer that they would operate as efficiently as Copart in a catastrophe, something they are unlikely to be successful at. In fact, Copart gained share through Katrina and in the aftermath as insurers understood to not just pick a salvage vehicle service provider based off how they operate under normal circumstances.

In the aftermath of Katrina, they bolstered their land holdings, keeping empty lots nearby that could service the extra volume from CAT events. After deciding several years ago to outsource their trucking fleet since it was cheaper, more efficient, and allowed them to side-step union issues that were bubbling up in Michigan, they decided to partially reverse that decision and keep some owned vehicles. These vehicles would only be used when there was a natural disaster that resulted in local operators exceeding capacity, so Copart could service their clients without having to pay usurious rates or pay to source providers nationally.

By the end of fiscal year 2006, Copart had 122 locations and over half a billion in revenues with software-like operating margins of 32%. Revenue over the past 14 years grew at an incredible 37% CAGR. However, that was largely driven by acquisitions, many of which were paid for in stock. Still though, revenue per share—which incorporates dilution of shares growing ~13x their 1992 amount– grew 14% annually.

With ~35% market share of the domestic market, Copart started looking abroad for new markets to apply their model to. In 2007, they entered the UK market through publicly listed Universal Salvage, who operated seven locations. They estimated that the UK market was 600,000 salvage cars annually with Universal Salvage the largest player with 20-25% market share.

In 2007, Universal Salvage made just £3mn on over £70mn of revenue. This is a mere fraction of the profitability Copart runs at. This is partly owing to a smaller and less refined operation (they were in the midst of a turnaround), but also because the UK market was run the way the US market used to be, with salvage operators buying the cars from the insurance carriers instead of selling the cars on their behalf. It would take several years to prove to the UK carriers that their methodology of cleaning the cars before auction and sharing the revenue of the sale would boost their returns and eliminate the insurers incurring losses on cars whose transit fees were greater than auction sale price.

When Copart entered the UK, they connected their international and domestic businesses, making the marketplace all the more vibrant. UK buyers could not only bid on the local supply, but now also access cars all across the US. This cross-seeding of marketplace supply and demand drove returns higher for the insurance companies as bid density drove price discovery. Competing salvage auctions were at a further disadvantage since they not only lacked a buyer base that was over a hundred thousand strong, but also the technology to run online auctions. In 3Q10, Copart disclosed that unique buyers in the UK increased over 94%.

While they worked on convincing insurers to convert to their PIP model, Copart continued to expand through the financial crisis, acquiring four more facilities in the UK in 2008 and five more in 2010.

When the financial crisis hit, the business was in good shape. As Jay noted on the 1Q09 call: “we are in the best competitive position that we have ever been as a Company. Copart has no debt. We have $50 million in cash… We’ve got the best network of facilities and we’ve spent the last decade building that network.” Their strong position was buttressed by the auction dynamics which can compensate for weak car prices with more car volume. This is because the lower the car’s resale price is, the more cars the insurance company decides to scrap instead of repair (more on this dynamic later).

The net of all of this was that a financial crisis that pushed GM and Chrysler into bankruptcy resulted in nothing more than a dent to Copart’s financials: revenues and operating income contracted 5% to $743mn and $225mn, respectively. In the meantime, they were preoccupied with re-architecting the website experience. Instead of forcing users to become members in order to view vehicles, they opened up their site to allow anyone to browse cars. The outcome of this near immediate, as just a few quarters later, in 3Q10, Copart noted that they had signed up over 200,000 new members.

While their site traffic was booming, they announced another significant development: their RFP (request for proposal) to Allstate was accepted. Copart would be the exclusive national provider of vehicles sales and auction services for one of the largest insurance companies in the US.

With the business in strong shape, Willis officially stepped down as CEO after 28 years, passing the reins over to Jay, but remaining the Chairman of the Board of Directors. After a childhood of learning to live off literal scraps and living in junk yards, Willis’ 6.7% stake in the company makes him worth over $1.1bn.

Copart would continue to grow their reach, improve operational efficiency, and strike new supplier agreements with insurance companies. With ~40% market share in North America, they have embarked on an ambitious growth plan to dominate the foreign salvage auction market with budding operations in Germany, Spain, and Brazil, among others. They have grown operating income almost 5x since Willis left, closing 2022 out at almost $1.4bn. Jay is 53 years old today, almost a decade younger than Willis when he left. How much more can Copart grow under his tutelage, and could they ultimately be the clear dominant leader in this market globally?

Business.

Copart is a global provider of online auctions and vehicle remarketing services with a focus on salvaged vehicles. ~80% of Copart’s vehicles are procured from long-term supply agreements with insurance companies who rely on Copart to arrange the pickup, storage, title processing, and selling of vehicles that the insurance company deems a total loss. This is a critical service for insurers because Copart not only helps ease the logistics of dealing with salvaged cars but helps them get the highest return on their vehicles. The higher the auction proceeds the insurer receives, the more their expected losses drop, which allows them to price their policies more competitively. The other ~20% of Copart’s vehicles are from vehicles that are repossessed from banks and financial companies, as well as charities, fleet operators, dealers, vehicle rental companies, and individuals.

Copart arranges to pick up the vehicles and store them at one of their ~250 locations. Depending on whether they are enrolled in the PIP (percentage incentive program), Copart will clean and vacuum the cars, then take photos. When the photos are posted, registered members can bid on the cars in an online auction that typically lasts one week. The winner of the auction is responsible for arranging the transportation of the vehicle, but Copart helps connect them to many local service providers. Exactly what an insurer gets charged for depends on their contract, but it could include taking a % of the total sale price (PIP), and/or storage, processing, titling, and other fees.

Copart has two operating segments: US and International. The US segment is responsible for 84% of revenues with international making up the rest of the 16%. However, international buyers are an estimated ~35% of vehicle sales.

Service Revenue consists of auction and auction-related fees charged for vehicle remarketing services. Depending on the particulars of each contract, auction-related selling fees can be based on a percentage of the vehicle sale price, tiered vehicle selling price fees, or a fixed fee based on the sale of each vehicle. Other fees may include transportation fees, title processing, preparation fees, vehicle storage fees, bidding fees, and vehicle loading fees. Critically, everything in the “service revenue” segment is recorded net of the vehicle cost. (I.e., the total revenue generated per car is netted against the proceeds given to the seller). Bidding fees, as well as an annual membership fee for the right to become a bidder, are borne by the bidder.

Vehicle Sales pertain to certain vehicles that are purchased and remarketed on their own behalf. This is typically the byproduct of differences in how national insurance markets work (more on this later), as well as their small operation of buying cars directly from individuals. Since Copart is a principal in this transaction, they record these vehicle sales on a gross basis with “Cost of Vehicles” itemized in their operating expenses. While it is true that the risk profiles of these transactions are slightly different, we think it makes more sense to look at these vehicle sales net of the vehicle costs. (The next financial table recharacterizes these transactions on a net basis)

Below, we show part of Copart’s fee schedule. The buyer fee increases corresponding to the final bid price and whether it is a clean or non-clean title.

In addition to the buyer fee, there is a $79 gate fee assessed on all purchases, as well as a “virtual bid fee” for each online bid placed. There are other fees that can be assessed like storage fees on pickups that take longer than one week, environmental fees, and if members use a Copart-affiliated 3rd party finance solution. Additionally, in order to bid on a car in the first place, buyers must become a member, which costs $99 annually (premier membership is $349, which allows a buyer to bid on more cars at once). The seller fees (i.e., what insurance companies pay) are more opaque, and every contract differs.

While that may seem like a lot of fees, there is a high cost associated with moving the vehicles and storing them. But no doubt Copart and competitor IAA (who has a very similar fee schedule), both share pricing power on the buyer side, who has little leverage in the relationship. The two companies sell ~90% of all salvaged vehicles, giving buyers few alternatives. The largest buyer, LKQ, has made some efforts to go direct to the insurance company, but this has largely failed for reasons we will get into later.

The fee to bid virtually may seem odd since eBay and other online auctions make bidding free in order to drive up bid density, but this is largely a vestige of the fact that the virtual bidding fee was in place of paying a 3rd party to visit a yard on the buyers’ behalf. Also, the industry dynamics are such that the buyers need to access the supply more than the suppliers need any one buyer, and there is no risk of a new supplier coming online (more on this later).

Returning to their financials, we adjusted revenue to net cost of vehicles against vehicles sales to get a more accurate portrayal of revenue without the 1P vs 3P distortion.

We see that on a net basis, Net Vehicle Sales dropped to 2% of total revenue from 19% prior. This more accurately reflects its economic contribution.

Below, we see revenue by geography mix (net adjusted). On this basis, the US contributes 88% of revenue, whereas international operations contribute just 12%.

Copart’s LTM revenues of ~$3bn have grown ~16% since 2015 and 19% since 2021, as Covid induced supply chain issues increased car prices across the board.

Copart’s revenue growth is driven by a mix of increasing totaled cars (salvaged car TAM growth), market share gains, and increasing revenue per unit.

The drivers of salvage cars are 1) miles driven, 2) accident rates per mile, 3) and the salvage rate.

Looking at these three factors, two of them have continually trended up over time: 1) miles driven and 2) salvage rates. Miles driven has grown on the back of more people owning more vehicles and general population growth. In 2000, there were ~2.7tn miles driven annually vs 3.25tn today, which is ~1% annual growth.

The larger driver of the total number of salvaged cars increasing is an increase in salvage rates or total loss rates, which are cars totaled divided by all insurance claims in a given year. In the next section we will detail the decision process of how a car becomes “totaled”, but in short, if the vehicle is too expensive to repair, they total it. As cars have gotten more complex with sensors, advanced electronics, and other safety features that need to be reset, like airbags, repairs have become much more expensive over the past several decades. Since the 1980s, total loss rates have increased from ~4% to ~20%.

This is a trend that is expected to continue as vehicles continue to get more complex. Offsetting the increase in miles driven and salvage rates though, is a lower accident rate per mile driven. Better vehicles that can stop quicker, and more recently, accident-avoidance technology, has helped decrease accident rates. However, these gains in better safety technology reducing the accident rate are slightly offset by more distracted drivers due to smartphones (the accident rate slightly increased for several years in 2011).

Newer cars have more advanced accident-avoidance technology with lane departure warnings, cameras, and beeping distance sensors. These reduce the accident frequency, but when there is an accident, it is more expensive to repair (hence the higher salvage rates). We will touch back on this in the next section, but at a high level, the number of vehicles that are salvaged has grown over the past few decades and has structural pressures that will likely drive it to continue to grow. Jay Adair has said he thinks total loss rates could go from ~20% to 35-40% in the future. (However, it is not clear how much that would be offset by fewer accidents with accident-avoidance technology prominence growing)

With the number of salvaged vehicles growing annually, the next piece of that equation is what Copart’s market share of those vehicles is. We will dive much deeper into this later, but right now, Copart and IAA basically have a duopoly on the market with ~90% share. We estimate Copart has slightly more market share than IAA (detailed later). As noted, market share gains have driven much of Copart’s historical revenue growth, but is likely to be a smaller factor going forward.

The last piece of the revenue equation is Copart’s revenue per vehicle sold. We noted their fee schedule earlier, but just to complete the revenue build, there are two aspects: 1) the revenue that varies with the average selling price of the car, and 2) the revenue that varies with volume of cars. Copart takes a commission from the buyer and seller, based off of the total selling price and also a fixed fee per vehicle. (Copart also has some other ancillary revenue from bidding fees and add-on products like extra pictures, but this formula accounts for the vast majority of their revenue. We also have only mentioned salvaged vehicles, which are ~80% of the cars they sell. The other ~20% is lower end, older cars that are heavily used, but do not carry a “salvaged” vehicle title. This portion of supply has stayed at the same portion of total vehicles for the last several years, despite insurance vehicle supply growing.)

The net of all of this is, at a high level, that Copart makes ~$1,000-1,200 in net revenue per vehicle sold. However, around $200-300 is for sub-hauling and tow storage that they forward on the insurer’s behalf. That leaves $700-1,000. If the average vehicle commission for buyers and sellers together is around 20% and if you include the bidding fee plus other fixed fees, that backs into an average vehicle selling price of $3-4k, which is in line with our industry checks. The average vehicle selling price increasing over time is one way Copart can continue to grow revenues (since they take a % of the sale).

Turning to profitability, margins have always been strong for Copart, typically exceeding 30% and averaging 33% in the last decade. There has been some volatility with margins owed to opening up new yards before they reach full utilization and CAT events where volumes swell, but profits are close to breakeven. Increasing ASPs, like we saw in the past year, also drives higher margins (but profit dollars are offset by lower volume).

EBIT has grown over the same period from ~$285mn to ~$715mn, representing a ~13% CAGR. EBIT margins (on our net revenue calculation) compressed ~500bps over the same period from 28% to 23%.

We will now dive into the industry and auction dynamics.

Industry and Auction Dynamics.

North America has about 275-300 million vehicles. We estimate about 10-15% of those, or ~28-45mn, file some sort of insurance claim every year. The total loss rate, which is vehicles salvaged divided by total insurance claims, has decreased over the past few quarters on higher car prices (a dynamic we will explain momentarily), but at a high level, have been in the vicinity of 20% (barring last year where they dipped). This means that one out of every five cars that has an insurance claim filed will be “totaled”.

Once a car is in an accident, the damaged car is usually taken to a temporary storage lot. This is more expensive than storing at IAA’s or Copart’s location, so if they immediately know it is a totaled car, they will try to take them directly there. Once the insurance company assesses whether or not to total the car (more on the decision of how a car gets totaled in a moment), the damaged car is taken to one of Copart’s or IAA’s yards. (If the car is not totaled, it goes to a mechanic). Copart and IAA both help arrange transportation to one of their locations.

Once there, they have to work on getting the car’s title ready, which can include making sure there are no liens on it from outstanding bank loans. If there is an outstanding loan, they have to get it released. Totaled cars have to have their titles changed to a salvaged title and are no longer allowed to be sold to anyone without the proper licenses (which vary by state). The title processing with the DMV is by far the longest part of the transaction. Copart even has system integrations with the DMV, but it still takes ~40 days to process the title. Depending on the insurer’s contract, Copart will then clean up the car, clear it of debris, and take photos to post for online auction. Once an online auction concludes, the car is sold to the highest bidder (unless the bid did not reach the reserve price). The car’s buyer then typically uses a Copart or IAA affiliate to help load and ship the car to them. The whole process takes around 60 days from car pick up to sending it out to the winning buyer.

The decision of whether an insurance company totals a car is a simple formula. If the value of the car after the accident plus the cost to repair the vehicle is more than what the car was worth before the accident, then it is totaled. Said differently, if the cost to repair the damaged car is more than what the car was worth right before the accident less the proceeds they can get for selling the damaged car, then it is totaled.

In the example below, we look at the decision of whether or not to total a 2018 Honda Accord with substantial damage. The ACV, which is what the car was worth immediately before the accident, is estimated to be $25k. After the accident though, the insurance company estimates the damaged vehicle will fetch $6k at auction. The claimant’s car is now worth $19k less. If the insurance company can get the car repaired for less than $19k, they will pay to repair it. If the repairs cost more than $19k, they will total the car. This means they effectively “buy” the car from the claimant for $25k and recoup $6k of that in auction.

Said differently, the insurer’s “max loss” on the vehicle is limited to the ACV less the market value of the damaged car recouped in auction, or $19k in the example. Then they will only repair the car if it is less than that “max loss”. Below, we see the flow chart that shows the three key parts that influence the decision to total a car: the ACV, the market value of the damaged car, and the cost of repairs.

Now, these three variables themselves have several variables that influence them. The ACV is impacted by everything from car prices, interest rates, car durability improving to potential supply chain issues limiting vehicle availability like we saw during Covid. The more expensive used cars get for whatever reason, the higher the ACV. All else equal, the higher the ACV, the more an insurer will be willing to spend on repairs before deciding to total a car.

The damaged value of the vehicle is impacted not just by used car prices, but also by the volume of salvaged cars and demand for salvaged cars. The demand for salvage cars is itself impacted by the price of cars, as rebuilders and repair shops are willing to pay more for car parts when they believe they can sell the finished product for more. Commodity prices are also a factor (mostly for low-end cars) as the price of a crushed car fluctuates with scrap metal prices.

We mentioned that total losses have generally trended up towards ~20%, which is up 5x over the past four decades. The key factor driving the total loss rate higher is more complex cars, which increases the cost to repair them. When the cost to repair a car increases, it becomes cheaper to total more cars rather than get them repaired.

Insurance companies look at accident frequency and accident severity. Frequency is how often accidents happen, whereas severity is how bad the accident is. With new technologies like bumper sensors and blind spot detectors, accident frequency has been dropping. However, when there is an accident, the repairs are far more costly. A car’s bumper used to just be a couple dumb pieces of material, but now it has a lot of wiring and sensors that need to be calibrated to a central computer, all of which increases the cost of a replacement bumper as well as the cost to install it. This increases the likelihood of a car being a total loss.

Insurance companies rely on Copart to help them get top dollar for their totaled cars, which in turn increases the likelihood they total the car. (In our example above, an increase in car auction proceeds would decrease that “max loss” of $19k, which means the threshold for how much repair cost the insurance company would be willing to bear is lowered). Copart also helps insurance companies estimate the value of a damaged car through their ProQuote tool so they can write more accurate estimates (IAA has a similar tool).

Copart reshaped the industry through their 1) PIP revenue model, 2) global online marketplace which helped improve vehicle price discovery, and 3) analyzingtheirlarge data set which helped insurance companies decide which cars to total. The impact of all of this was an insurance industry that monetized their salvaged cars much better than prior and thus was more likely to total cars in the first place, increasing the pool of salvaged cars.

Of the 275-300mn vehicles in North America, some 5mn+ are totaled each year. This is a critical source of supply for Copart (and IAA). About ~80% of Copart’s vehicles are sourced through insurance companies with long-term supply agreements. Each contract is heavily negotiated, and terms are seldom disclosed. Since the vehicle insurance industry is pretty consolidated with the top 10 players representing ~75% of the total market in North America, each contract is a material driver of vehicle supply.

Historically, insurance companies have relied on a vast array of local junkyard operators, but as Copart and IAA consolidated the industry, the choice is increasingly just between them two in North America. It is tough to get an accurate sense of market share, but we pieced together estimates by going through past earning call comments, competitive disclosures, and channel checks.

As a disclaimer, market share estimates are hard to size up because the “market” is never clear (does it include whole cars? Only low-end whole cars? Only the salvage units? Only top 10 insurers supply? What geography?). Nevertheless, we have to make an attempt as Copart’s future growth will come from either total market growth or market share growth. Historically, market share growth has been a large contributor to their increasing revenues, but if they already have a dominant position, then we would need to recalibrate our growth expectations. It is for these reasons we are forced to try to estimate the market and market share, whereas with other companies we can commonly assume the market size, or their share, will not be a limiting growth factor (especially when many great companies offer products that grow their markets).

Below we see CPRT unit sales volume, which they disclose on each earnings call. With the exception of Covid and distortions from CAT events (which inflate volumes in the period of the catastrophe), volume has always been positive. Indexing volumes to 2014, we see that their total volumes have increased ~80-90% over the past 7 years. This equates to approximately 9-10% annual volume growth.

As of 2019, KAR (prior IAA owner, more on this in the next section), disclosed that IAA had “approximately 40%” market share and that “IAA and Copart together represent over 80% of the North American Market”. While the careful wording of KAR does not preclude the possibility that Copart had a higher market share at the time, we will assume for this analysis they both had 40% market share in 2019. IAA disclosed their volume was ~2.5mn units and later they disclosed under their new owners (full IAA history in the next section) that their volume was ~2.3mn. In 2019, IAA lost significant volumes from one of their biggest carriers (GEICO) shifting volume to Copart, which is likely the biggest contributor to their volume loss.

Copart discloses that they handle over 3mn units annually, but that includes their larger international operations relative to IAA. Using Copart’s disclosed US volume numbers, and conservatively estimating that Copart and IAA had equal market share in the US in 2019, we think Copart’s US market share is around 47% and IAA’s has fallen to ~37%. We have seen other estimates put Copart’s market share as high as 60%, but that seems too high. There still are some local and regional players remaining, as evidenced by Copart’s on-going acquisition of US-based facilities. Exactly how many of these yards still exist is hard to size up, and while the large insurers almost certainly don’t work with them, there are still local and regional insurers. In some sense though, assuming Copart has a higher market share in the US currently is more conservative, because that is less volume they can possibly gain. We will pick back up on this, as well as international volume and market share, later on. With the exception of the UK, their international operations are in the early innings, and in the U.S., we should assume Copart is the dominant player with limited ability to gain further share.

Also limiting Copart’s ability to grow market share is the fact that there is a bit of a balancing act between insurance companies’ volumes, as they don’t want to be beholden to a single vendor. However, they all want efficient operations that allow them to earn the highest proceeds per car. IAA and Copart are by and large similar in this regard. However, Copart has typically gained volume from their superior ability to handle CAT events. As we noted, Copart doesn’t aim to profit off of CAT events, but rather use them as opportunities to showcase how they are a better-run and more reliable operation. While many insurers wanted to use Copart during CAT events, Copart will only take them on as clients if they signed long term distribution agreements.

The aftermath of Hurricane Katrina helped them win Allstate’s business, and years later, Hurricane Harvey (2019) helped them win GEICO’s supply. Nevertheless, despite Copart’s superior catastrophe performance, insurers still want IAA to stick around so they have some leverage over Copart. State Farm has said that they will redirect some volume back to IAA if necessary to ensure there are two viable salvage operators. (In a world where only Copart exists, Copart could drive their sellers commission rate much higher).

To better understand competition, we will dive more into IAA. While IAA and Copart have many similarities in how they function, IAA has disclosed more granular data, which helps inform on Copart’s business as well, as well as give us a better sense of the industry.

IAA.

IAA started in the salvage vehicle business in 1982 under the name Los Angeles Auto Salvage (LAAS). Similar to Copart, they embarked on an aggressive series of acquisitions to consolidate the industry. In 1990, all outstanding (private) stock was acquired in a leveraged buyout, and a year later they changed their name to IAA (Insurance Auto Auctions) to better represent their increasingly national footprint. They IPOed before Copart in 1991 and originally traded under the symbol IAAI. When they acquired a yard, they would often just leave it to operate as it did prior, instead of taking the time to train new employees to make IAA’s culture and operations more consistent.

There were other differences. In 2004, just 28% of vehicles were sold on the “percentage of sale consignment method” (IAA’s version of PIP). In contrast, Copart had 65% of their vehicles sold on PIP at the time. This was an underappreciated competitive edge Copart had, as PIP was proven to increase returns for the insurance company and eliminated vehicles whose sales lost the insurer money (that is, when tow and processing costs were higher than auction proceeds).

Whereas Copart ripped the “band-aid” off and moved to all virtual auctions in the early 2000s, IAA was still trying to balance being both an online and live auction as recently as 2020. Copart saw firsthand how trying to handle both was leading to operational inefficiencies and complexity so went to an entirely online auction. IAA instead would support both systems for decades, not moving fully online until Covid forced them to. We can take their delay of this decision and supporting two systems as emblematic of the institutional inertia any business changes at IAA would have to overcome.

All of these operational differences led to IAA being a much more inefficient operation, which shows up in the numbers. In 2004, Copart had an ROIC of >35% whereas IAA was <10%. Despite the two companies having similar sized operations, Copart’s 2004 pretax income was $130mn and IAA’s was $19mn. (Jay Adair on the 4Q04 earnings call noted that market share for Copart was around 35 to 40% at the time).

In 2005, IAA was taken private by two PE firms at a ~$385mn valuation. Several years later, in 2007, it was combined with the publicly traded ADESA, the 2nd largest whole car auction provider (whole car is any non-salvaged vehicle or used but not heavily damaged car). These two companies, along with a floorplan financing business comprised what became known as KAR. IAA effectively became public again.

IAA under KAR went from $165mn in gross profits in 2007 to $505mn in 2018. However, this was largely a result of acquisitions and the general industry’s growth. Copart gained share over that period with a few high-profile insurers switching over, including Allstate. Contacts who have worked with both companies generally comment on the slow response rate of IAA and lack of customer consideration compared to Copart.

Despite combining the companies just a decade earlier, in 2018 KAR proposed a spin-off which was completed in 2019. IAA was a standalone public company again, but not for long. A few years later, Ritchie Bros would make a ~$7.3bn bid to acquire IAA. The acquisition was completed in March 2023. If a common IAA criticism was lackluster customer service and slower responsiveness, it is hard to see how sharing facilities with another auction provider who services different customers and focuses on different machinery would help.

Ritchie Bros. talks about the cost synergies of combining their auction properties with IAA ($100-120mn in synergies) and how their “efficient yard operating model” alongside their “experience salesforce” will drive revenue synergies of anywhere from $250-780mn. It is not obvious why IAA wouldn’t have an “efficient” yard system after 4 decades in business or how adding new sales reps could improve their vehicle supply when that has always been a key focus of the business. This can either be taken as proof of IAA’s poor management, an indication of Ritchie Bros’ lack of understanding of the business, or just a Wall Street-focused acquirer trying to get investors excited. However, no plans were announced to have John Kett, the CEO of IAA since 2014, leave.

Rewinding 15 years, KAR said a similar thing about combining IAA with ADESA’s whole car auction. They thought that having two auction houses under one roof would be a better utilization of land, staff, and shared technology.

In reality though, it really meant a lack of focus and sub-optimal resource allocation to both businesses. During Kar’s ownership of IAA, they lost several large carriers to Copart. A decade later, KAR noted that a spin-off would mean “enhanced strategic focus”, “streamlined operating structure”, and “optimized capital allocation”.

Now, Ritchie Bros is using a line of reasons similar to the one KAR used to justify their IAA acquisition. To be fair, while KAR may not have benefited much from synergies, Ritchie Bros’ merger rationale isn’t without some merit. In theory, it makes sense that having more land and more product to push through that land could lead to better utilization and lower transportation costs. Ritchie Bros notes they have a lot of deadhead space from tow vehicles and flatbed trucks, which is when a transporter only carries a load one-way and drives back empty. In reality though, mixing products and business lines is just as likely to lead to new operational hiccups and further customer experience degradation.

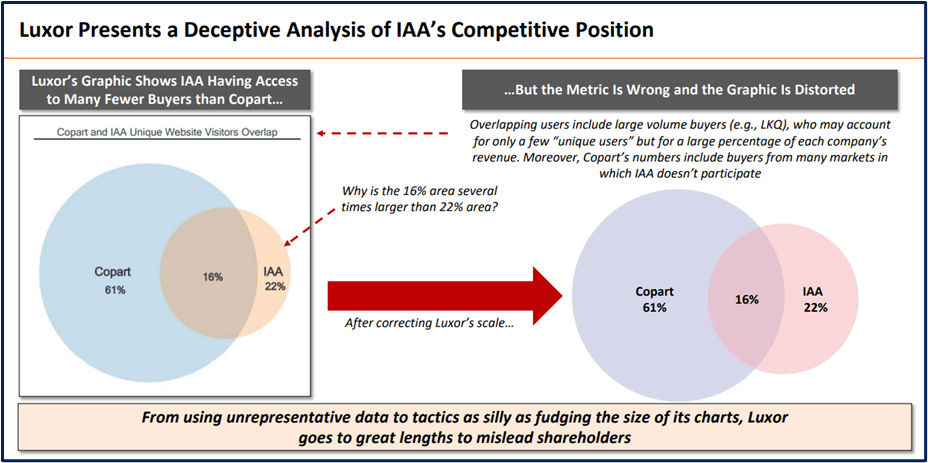

Shortly after announcing the $7.3bn IAA acquisition (compared to Ritchie Bros’ market cap of ~$6bn), a large shareholder, Luxor Capital, launched a campaign against the deal. They outlined some of the issues with the deal rationale, notably that Ritchie Bros’ yards are not zoned for salvaged vehicles and the idea that Ritchie Bros’ international presence can drive IAA growth is misplaced as the model is very different from North America (consumers typically retain vehicle ownership after an accident; more on this later). (Luxor’s biggest complaint seems to be that Ritchie Bros is a much better business, and they don’t want to dilute that with what they see as a second-rate marketplace).

In response, Ritchie Bros put out a 68-slide presentation detailing various benefits, synergies, and opportunity for valuation “re-rating”. Within the presentation, they had a 26-slide section labeled “addressing investors’ concerns” to rebut Luxor’s claims. There are several specious “potential drivers” like IAA attaining a “50/50 market share split” through “differentiated offerings” and “enhanced CAT resources”. What these differentiated offerings are remains unclear, and as Copart built their reputation through a vastly superior CAT response, it is unlikely anyone will move to IAA just because they buy more trucks. Ritchie Bros also notes the whole car sales opportunity, but IAA was just spun-off from KAR, whose subsidiary ADESA was solely focused on whole car. If going after whole car was that easy, IAA would already have benefited from some of the knock-off effects when they were the same company.

In the slide below, Ritchie Bros’ management even takes issue with the size Luxor presented the pie charts, noting that the circles should have been less overlapped. Ritchie Bros does not dispute the numbers on the chart, just how the circles are depicted, and they recreated the graph shown on the right. (Luxor was making the point that IAA has worse marketplace liquidity than Copart because of fewer international buyers. However, in our channel checks, the proceeds the insurance companies received from either Copart or IAA were claimed to be largely similar. Ritchie Bros probably should have rebutted the claim by showing auction proceeds are similar instead of worrying about how overlapped the circles are).

Accompanying this analysis is a slew of sell-side quotes on how they approved of the Ritchie Bros deal. While we understand that management was trying to dispel the assertions an investor was making, it shows how Wall Street and narrative-focused they are (and of course, sell-siders are far from unbiased, as they rely on corporate access). While it is not always true, more often than not, managers who focus too much on what Wall Street thinks are too short-term oriented and don’t spend enough time on managing their business. They tend to factor into their decision-making how something “looks” to financial analysts rather than what actually makes the most economic sense. (We think this is part of the reason that IAA leased rather than bought their land and calls out “extraordinary” events from CATs, whereas Copart considers them a normal part of business).

Copart, in contrast, has only ever released one slide presentation, and it looks like an intern could have made it. Founder Willis Johnson has never spoken on an earnings call. Jay Adair also stopped speaking on earnings calls several years ago. Copart is not trying to impress Wall Street so much as just explain their business.

To Ritchie Bros’ credit, they have compounded earnings at a 14% CAGR since 2000 (and since IPOing in 1998, have outperformed the S&P 500, earning shareholders a ~8.5% return before dividends). Nevertheless, they have given away almost half of their company in this mostly stock transaction, making it the single most important transaction in their history.

Founded in 1963, Ritchie Bros has only in the past seven years embarked on sizeable acquisitions. And even then, they have been a magnitude smaller than the IAA acquisition. Over the past few years, they have acquired IronPlanet (a used heavy equipment marketplace), Mascus (a leading online equipment listing service), and a few smaller international auctions. IronPlanet was their largest acquisition at the time in 2017 at a price of ~$750mn. A year after that acquisition, in a 4Q18 earnings call, then CEO Ravichandra Saligram noted “pure-play volume in 2018 significantly exceeded the pure-play online volume generated by IronPlanet in its peak year of 2016 as a stand-alone company”, suggesting the acquisition was a success. Other commentary also seems to suggest they viewed this acquisition positively, but despite this limited success with a prior acquisition, IAA is a magnitude larger and in a different industry.

It is also worth noting that Ritchie Bros has a very new management team with limited direct experience in salvage auctions or even their core marketplace industrial/commercial offerings. Most managers have been there just since 2020 and several (like the CFO) just since 2022. At the end of the day though, IAA operates in a very favorable industry with clientele who do not want to be captive to a single provider, and thus willing to cut them some slack. However, as it pertains to Copart, it does not seem they have much new to worry about.

Copart Model.

Copart Model.

To comprehend how integral Copart is to the inner working of the insurer’s disposition function, understand that insurers have to transport and find a place to store 10 totaled cars every minute. And totaled cars can leak dangerous chemicals, so they need to sit somewhere for upwards of three months. It’s not feasible to centralize the storage locations because it is far too costly to ship cars across the country, so they need localized storage to keep towing costs down. However, there are zero cities or people that want literal junk yards near them, which makes securing permits for new lots a multi-year process, at best. And that is only if you can find the land—in some of the most populous cities, whether it be Los Angeles, Miami, Chicago, or New York, it is near impossible to find multi-acre plots of land close to the city center. However, even finding land in one area isn’t good enough anymore, because competition has moved to serving on a national scale.

Not only does having more plots reduce the cost to tow, it also allows for more car storage, which increases the pool of cars the auction can offer. This in turn increases the buyers they attract—a critical factor in making sure each car has the bid density to ensure a fair market value. To replicate this would be difficult—most of the land Copart owns was bought decades ago at much lower valuations and with salvage yard permitting that may never be granted again in a given area.

The more yards they have, the more the transportation coordinating function moved from the insurance company to Copart. No longer does an insurer have to manage a list of hundreds of different local junkyard providers to direct vehicles, they now have the option of only working with a single one: Copart. Copart in turn can handle all of the logistics of moving undrivable cars across the nation.

The more insurers that sign vehicle supply over to Copart, the more they are able to rationalize further yard purchases, building more regional density. This drives operational efficiency in terms of reduced tow times and lower costs. Larger yards with high yard utilization spreads the overhead across more vehicles, reducing storage costs.

But securing an insurer’s vehicle supply does far more than enabling yard growth—it drives marketplace liquidity. The more vehicles Copart secures, the more buyers flock to their site. The more buyers on their site, the more salvaged vehicle prices increase as incremental buyers drive price discovery. This is all buttressed by their extremely early introduction of online auctions, which moved car bidding from an inherently local process to not just a national one, but a global one. ~35% of vehicles are now sold internationally. In fact, if an insurer doesn’t get a certain amount of bids from, say, the UAE or Estonia, they won’t lift the car’s reserve for fear that it is not getting a fair market value. As Copart opens up new international markets, this cross-border network effect is only strengthening.

Copart doesn’t just have long-term supply agreements with insurers, they have direct integrations into their ERP systems. The insurer computer talks to Copart’s to easily monitor their tens of thousands of vehicles that are sitting in inventory across the country and gauge vehicle returns. Copart also has a direct integration with each state’s DMVs, which differ in regulations, in order to help expedite title transfers. These integrations are not just hard to replicate, but allow for total transparency in the vehicle processing.

The millions of annual car sales Copart facilitates gives them a further advantage—they have the best salvaged vehicle data of any single provider. Insurers do not just rely on them to move the vehicle and sell it, but utilize their data through Copart’s PriceQuote tool to help inform what cars they total or repair.

It is no longer enough to have a single well-placed yard in a city with local insurer relationships in order to win business because competition is now national and global. A newcomer would need to be able to acquire hundreds of multi-acre plots across the country simultaneously—all with the correct zoning—just to begin. Copart acquired their land holdings over a 40-year period, and that was when the industry was totally fragmented and environmental standards were far laxer. Even if a newcomer could build the yard footprint, it is essentially impossible to see how they can wedge the large insurers, who represent over 75% of supply, from Copart and IAA. A newcomer wouldn’t have the buyer base that would make them a consideration, and without the insurers’ supply, it’s hard to see how they could possibly build a large buyer base—let alone a buyer base that is as high quality as Copart’s cross-border one. Even with buyers though, they wouldn’t have the insurer integrations, data sets, and perhaps most importantly—the reputation.

Copart gained the most supply by proving themselves through severe CAT events, which takes a very competent and prepared organization. Copart now reserves land just for CAT events, as well as keeps excess equipment in storage. This isn’t just a matter of being prepared, but actually having a functioning organization that can deal with demand surging 10x what they typically process.

From the land to the permits, long-term supply contracts, marketplace liquidity, integrations, and reputation required, it is hard to see how there will ever be another player in Copart’s core markets. So long as car manufacturers manufacture cars and insurers insure them, Copart and IAA will sit in between.

Copart vs IAA.

IAA had a lead on Copart in the 1990s, but today that position has flipped. While market share stats are hard to come by, we estimate Copart has an advantage over IAA. As mentioned previously, at the time of IAA’s spin-off from KAR, they noted that IAA is “one of the two largest providers” and has 40% market share. Putting that together with Copart and IAA’s disclosed statistics makes us estimate that Copart has ~10% more share than IAA today, or about ~45%. However, we have seen estimates as high as 60% for Copart (which we think is too high).

Copart is very tight-lipped about market share though, and the definition itself can be manipulated whether you are just considering all salvaged vehicles, just insurer supply, or including repos and old, low-quality vehicles. As mentioned previously, while understanding Copart’s current market share position is important to gauge the plausibility of further share gains, we do not think there is enough available info to make any high confidence assertions.

We do have a better sense of how these two companies differ though. IAA gets worse marks on customer service, technology, and organization. Insurance adjusters who visit the lots commonly complain that IAA’s vehicles are not where the computer system marks them at, whereas Copart is highly effective here. Copart was a leader in engineering the online auction, whereas IAA had a hybrid model until Covid forced their hand. Copart’s early focus on online auctions helped drive a much wider bidder base that is far more global than IAA.

From what we have gathered, Copart’s culture is also far stronger, with employees better at executing and serving customers with a sense of expediency. Since Willis Johnson laid out Copart’s “job” decades prior, Copart has remained focused on serving the insurance companies. IAA in theory does the same, but in practice insurers complain that they have trouble reaching customer service reps. Even internally, IAA employees complain they have trouble getting service reps on the phone to help solve a customer’s query.

Not that any of this is impossible to fix, but issues seem to stem from decades prior when IAA was content to leave newly acquired auctions alone instead of bringing them into a coherent and unified system. In contrast, Copart’s newly acquired yards had to learn the Copart way with strict KPIs that are monitored for every task from picking up a car to getting it off the lot and into a loader. Copart built out an ERP system to monitor all of their auctions in the 90s, which would allow them to identify underperforming yards and vehicle turnaround times. This early adoption of technology to monitor and improve operations helped drive efficiency and keep employees accountable, an important aspect that still drives culture today. Jay Adair even went on a cross country national trip in 2005 (dubbed the world tour) to try to meet all of Copart’s managers at each of their yards.

On the buyer side, the experience is fairly similar today. Whatever features Copart rolled out, like virtual 360 view, IAA has quickly copied. Some buyers even say that they prefer IAA’s UI to Copart’s, but that could just be a byproduct of using one more than the other. Either way, we consider the buyer’s experience on both platforms as roughly the same with the exception being customer service help, in which case Copart is better.

As far as pricing goes, buyers balk at the many fees both companies charge, but since Copart’s and IAA’s fee schedules are similar, it is not a point of differentiation. At the end of the day, buyers have basically two options to buy large amounts of salvaged vehicles. Since there are hundreds of thousands of buyers, but only dozens of insurance companies, the insurers will always have more leverage in the relationship.

LKQ, a publicly traded dismantler and seller of used vehicle parts, has tried to procure vehicle supply directly from the insurance companies, but has not been successful. The problem is that even though they want to buy a lot of vehicles, they don’t want to buy all of their vehicles. The insurance carriers need to get rid of all of their supply and cannot just let one buyer cherry pick supply and stick Copart or IAA with the rest because then the terms of the contracts would change unfavorably. Recall that Copart takes a loss on a certain portion of vehicles because they know they will make it up with others. Contracting out with LKQ would ruin this arrangement, and Copart would charge more on those vehicles. The insurers have not wanted to do this deal because they came to the conclusion the incremental commissions they would save from paying Copart or IAA by selling directly to LKQ would be more than offset by the higher commissions Copart or IAA would charge them for cherry picking supply, as well as the higher costs of dealing with another party to coordinate.

Even if we assume LKQ could figure out the fair price to pay for each car without an auction, which itself is doubtful, it would be operationally inefficient to let LKQ take “first dibs” on vehicle supply. When there is an accident and the car cannot be driven off, it is taken to a local tow yard. The storage fees at these tow yards are very high, so Copart and IAA usually have agreements to pick up vehicles at local tow yards within a day. This is even if the insurance adjuster hasn’t inspected the vehicle to decide if it is a total loss yet. There are cases where Copart picks up a car and stores it, only to have an insurance adjuster inspect it and decide it is not a total loss. In this case, Copart will send it to a repair shop. Even in these cases where Copart is ultimately not auctioning off the car, the insurance company saves a lot of money by not paying for extra storage days at the tow yard.

Adding another step to this with LKQ or another direct buyer inspecting a vehicle before deciding to take it on could drive up costs and slow down vehicle processing. The insurance adjuster would need to see the vehicle before the buyer, and if the insurance company doesn’t have an agreement with Copart to contract out all of their supply, they are not going to want to be quick with tow yard pickups and flexible with vehicle storage since they are not going to have the right to sell the car should it be a total loss.

Lastly, Copart pays tow storage fees and sub-haulers on behalf of the insurance companies and only recoups these expenses when the vehicle is sold. This is another dynamic that the insurance companies like and maybe would change should another buyer be given priority over Copart. Other than saving a small slice of commissions (each contract is different, but we’ve seen insurance companies pay up to 6.5% seller fees, but as low as 1%), the insurers do not gain much.

For these reasons, buyers have little bargaining power and are beholden to the duopolistic pricing structure. IAA could, of course, lower buyer fees to try to gain more buyers, but there would be no real incentive to do so. Adding more buyers to the auction is unlikely to drive up vehicle auction prices, so IAA would be left with less revenue. Copart may be forced to drop fees as well, but their higher margin profile means damage would be felt disproportionately to IAA. Copart’s larger international bidding audience, who bid from areas where IAA does not operate, means that Copart would be even more insulated from IAA fee pressure as many international buyers do not have IAA as an alternative. This is why historically IAA and Copart have never competed on buying fees (which represent about ~2/3rds of revenues). Instead, they compete on the insurer side for supply and by increasing their service level to both suppliers and buyers.

All of IAA’s issues have not been helped by regular ownership changes. They have moved from public company to a private business to a public subsidiary of a conglomerate to a stand-alone public and back to a private under a new budding conglomerate. This is in contrast to Copart’s almost comically consistent management and ownership structure: Willis Johnson has been the largest single shareholder since founding Copart, and they have only had one CEO ever leave, which was when Willis passed the reins down to Jay Adair.

Beyond North America.